Financial planners continue to be in the news – gosh, we must be an interesting lot. The focus of late has been on insurance – it’s costs and the differences between good and bad advice in this area. This is a short post, with a link to commentary from three different planners operating in the area of insurance advice. Each planner tackles advice for insurance in a slightly different way, and for anyone who is interested in the current debate and how it could play out, these articles can form a valuable insight.

Financial planners and insurance

As mentioned in a previous articles here and here, life insurance is not an area that all financial planners are involved in, yet most people will hold some form of life insurance cover either for themselves or someone else at some point in their lives – so it remains a central pillar within the financial planning world. The current news revolves mainly around a few key areas:

- ASIC’s release of a report into the quality of advice provided to people looking to obtain life insurance cover (covered in my post here)

- The Trowbridge Report – an investigation into ways of dealing with insurance cover and advice, and

- The difficulties facing insurance companies recently. While not as visible in the news cycle the fact is that insurers are having trouble remaining profitable in the face of major changes within the industry.

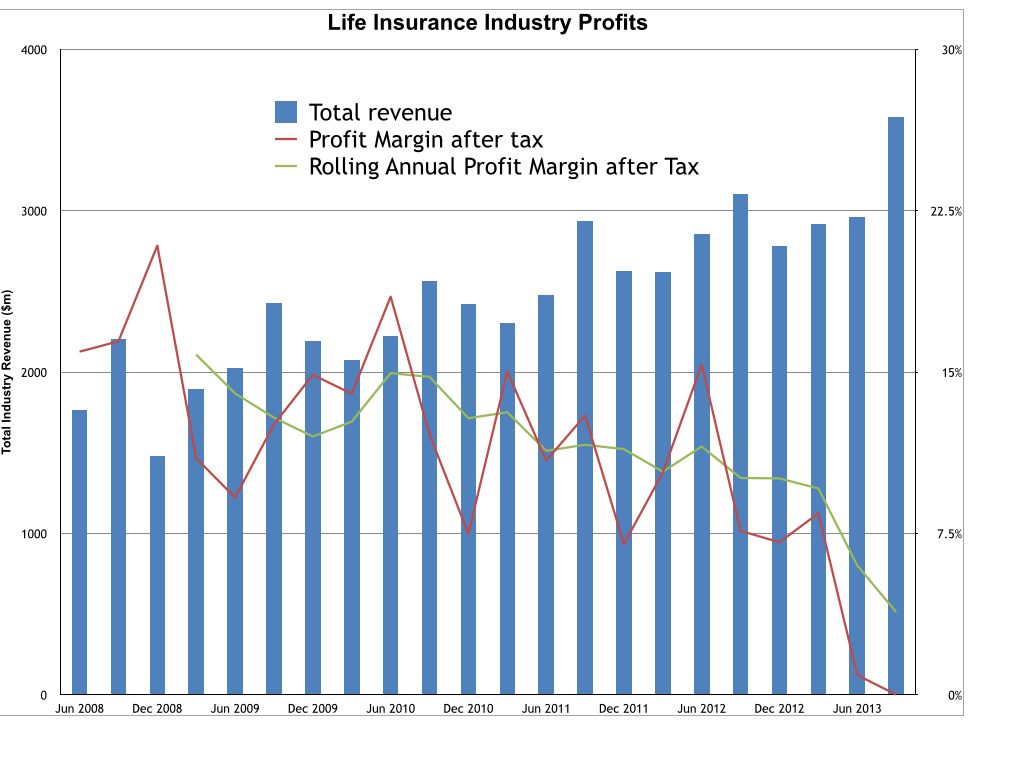

Insurance companies aren’t making enough money

A lot of people aren’t going to care too much about the profitability of some large insurance institutions but a huge number of people are impacted when that profitability takes a dive. If you didn’t have time to look at the link provided above, here’s one of the key graphics that presents a fairly good overview of just what has been going on…

The difficulties of life insurance companies are manifold. Claim payments are rising at a higher rate than assumed, and companies have found it more difficult to pass their risk onto other (usually) global insurance companies. A good deal of the problems are compounded in the “group” insurance area – which provides cover to members of large superannuation funds and other institutional clients. The result has been a large increase in premiums or/and changed terms of cover when those super funds or institutions were next due to renew their overall terms of cover. Nobody likes to see their insurance premiums rise dramatically but sometimes it’s simply a case of competition driving companies to offer premiums at rates lower than they should – so when the adjustment inevitably comes along, it hurts all the more. Here are two links to articles that cover some of these issues driving premium increases.

“Who’s driving up your life insurance premium?” from the Sydney Morning Herald, and “Insurance set to spike as new KPMG, FSC data shows mental health claims rising” from the website www.brisbanetimes.com.au.

ASIC’s report on the quality of insurance advice

ASIC’s report was a well-researched and in-depth look at whether financial advice for life insurance is being delivered at an appropriate standard. The overall report outcome was that while some advice was acceptable, there was too high a proportion of advice that was inappropriate, inadequate or just plain wrong. While the report highlighted a number of areas that should be looked at further, the main public debate flowing from it was fixated on the commissions paid by insurance companies to advisers who submitted insurance applications, and the potential that provided for advice to be in the adviser’s best interest rather than those of the person seeking advice.

The Trowbridge Report

The Trowbridge report is an interesting development. In effect, the proposal is that government will mandate the costs for providing advice – in effect converting an open marketplace into an area of fixed income against spiralling fixed and variable costs. While i find the idea interesting, the fundamentals underpinning it are not viable from a financial planner’s point of view without some fairly radical changes to how they deliver life insurance advice.

And so we come to input from people other than myself.

As usual, i welcome your comments, criticism (well, maybe not criticism so much) and feedback.

Michael

And a quick little aside…