Sharemarket cycles can be scary things. Most people know sharemarkets go up and down, and sometimes those moves can be savage. The nightly news will always highlight a large fall in market values, and news articles often highlight that “$x billion has been lost today” or some such wording. What is not so common however, is news reporting of the recoveries from such falls.

So today’s task is to look at two very large sharemarket cycles. We will look at two big market crashes and compare the post-crash recoveries. Doing so will help highlight how sharemarket cycles work, and how today’s seemingly ‘different’ times are usually just a repeat of what has already happened in the past. We can also ask ourselves whether the returns of sharemarket investors in today’s post Global Financial Crisis (“GFC”) world differ from those of earlier periods.

Why is that important and why am i sharing these thoughts? Well, it’s not just because i am a financial planner and we planners are cursed with a morbid love of charts and stuff. It’s because anyone regularly tuning in to the ‘noise’ of investment markets and news commentary would gain an impression that we are under some ‘strange new times’ and that post the GFC, everything in the money world is somehow different. Yet i am going to show you how the post-GFC world is not really all that different from the past.

Sharemarket Cycles

So are sharemarket returns lower post the Global Financial Crisis? Is it really ‘different this time’?

I don’t think that it is.

There are many reasons why people may suggest that the post-GFC world is ‘different’. However, the real reason has less to do with this or that fact, and more to do with our very human habit of interpreting the past through our current mindset. In other words, we ‘remember’ events and experiences differently, depending upon our current thinking. The lens most Australians look through today is one based on a 24-hour news cycle and a massive increase in the flow of facts/figures/opinions that impact on the average person in a way not even considered back in 1987 – the date of the last major sharemarket fall that i am going to make comparisons with.

It is my opinion that financially unaware people as well as financially literate people are gathering a set of ideas and thoughts on investment markets that are not necessarily accurate. For those interested in the psychology of interpreting events and decisions, here’s a link to Daniel Kahneman’s brilliant essay, “Maps of bounded rationality: a perspective on intuitive judgement and choice“.

A QUICK DISCLAIMER : Naturally, this opinion of mine is to be taken with a grain of salt, and you must not use it as a basis for making an investment decision, and past returns are no indication of future returns and anything i say is just an opinion and of no use to you at all, and many Very Clever People would disagree with me, and … ummm.. i think that’s about enough disclaimers for the moment.

Comparing Sharemarket Cycles

Over many years, i have maintained various tables and lists of sharemarket and economic variables. Once upon a time this was necessary, as obtaining such data and information was difficult or expensive or simply not possible for anyone outside of a large institution. Today i keep these charts and tables up-to-date because the habit helps remind me of how sharemarket cycles work, and how easily we can be led to think that today is somehow different.

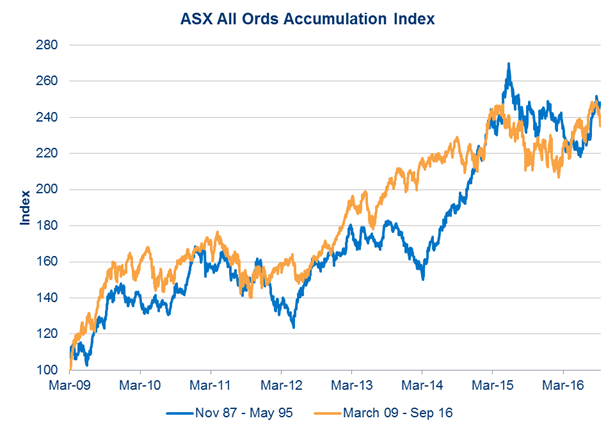

One of the charts i have maintained is a comparison of the 1987 sharemarket crash recovery period against the 2009 post-GFC recovery period. I have not shared this chart, as it’s based on my own figures and it could have included errors or omissions, and my precise mind didn’t like that idea. However, I recently attended an update by the fund manager Schroders, and the National Account Manager Chris Boyd was good enough to provide me with a copy of the chart presented. The good news for me was that the chart did reflect my own figures – but now I could point to a higher authority for the end result. In this case, Chris confirmed that Schroders had obtained the source chart from Bloomberg.

Thanks to Schroders for the chart provided here [source : Bloomberg]

So let’s spend a moment or two looking at what this chart may be telling us…

Firstly, it is based on the All Ordinaries Index plus dividends – ie, the ASX All Ordinaries Accumulation Index. So it is a pretty good representation of the broader Australian sharemarket. There were some changes to the index over that time – back in 1987 the “All Ords” represented the top ~300 companies listed on the Australian Stock Exchange (“ASX”). In April 2000 the range was expanded to the top 500 companies. So even with the changes, the ASX All Ordinaries Accumulation Index is a very good representation of movements in the overall Australian share market.

Sharemarket cycles – Crashes!

In 1987 the ASX suffered it’s largest fall in a single day – losing 516 points – or 25% (!!) on the 20th October. The index suffered a total fall of 43.9% from its October high to low points. So in the chart, the November 1987 blue line represents the All Ords after that low point.

Move forward to 2007 and the Global Financial Crisis starts grinding its way through global markets. The All Ords falls from 6873.2 right through to 3090.8 in March of 2009 – a fall of 55%. So the chart starts the orange post-GFC period from March 2009.

These were two very large falls in the Australian sharemarket, and were devastating to many sharemarket investors at the time. However, we are looking at sharemarket cycles, and that involves looking at both the crashes AND the recoveries. So the chart is focusing on the post-crash recovery periods and seeing how they compare.

Has a sharemarket cycle repeated itself?

You can see that the usual gyrations take place, with daily, weekly and monthly movements in the overall sharemarket index being very erratic. This is a logical outcome, as investors try to work out whether markets will keep falling or start to rise again. There would be people buying what they hope will be a bargain, as well as those who are selling shares they thing are fully valued or have little hope of making a reasonable gain from then. There would also be people selling simply because they had to or because their situation had changed. However, the gyrations in both cases show a gradual recovery from the post-crash low points.

If you look at the final few years, you will notice that both index lines begin to taper off a little.

For those with an interest in history and quirky coincidences, the rise through to a 1993 peak was brought to an abrupt halt by the US Federal Reserve lifting interest rates. As you can see from the orange March 2009 – Sep 16 line on the chart, the ASX All Ords has experienced a period of recent weakness, also brought on by talk of the US Federal Reserve lifting interest rates. I’m simplifying things a lot there, as other factors have impacted, such as China’s growth slowing, and worries about the potential fragmentation of the EU but the timing of interest rate changes is eerily similar.

Sharemarket cycles – rhythm or rhyme?

One of the key disclaimers required for any financial data that looks at past returns is the requirement to confirm that “previous returns are not indicative of future returns” or some similar wording. The Australian government regulatory body ASIC (Australian Securities & Investments Commission) has spent considerable effort in thinking through the use of past performance in advertising, and for the nerdy among us there is an excellent discussion paper available here. I include this link as I want to make it very clear that I am not suggesting that the correlations shown in the chart will continue. Nobody knows whether that would be the case or not.

Future returns certainly do not have to reflect past returns but in considering past returns then a comparison needs to be made somewhere. My interest in looking at this post sharemarket crash data has been fostered by an impression that many investors are seeing the post GFC period as somehow being ‘different’, and to my mind this is an impression that needs to have caveats placed on it.

There is no doubt that the incredible expansion of central bank balance sheets since the GFC is unprecedented – so in this case, it actually is “different” this time. In the post 1987 period huge changes occurred in global politics, with the fall of the Berlin Wall, Glasnost and the virtual end of the Cold War. Some economists argued that this brought about a “peace dividend” that encouraged investment and the opening of new markets and enhanced globalisation. The post GFC period has seen totally different changes, with globalisation being brought into question and Cold War tensions resurfacing.

Yet even with the huge disparity in events and economics and politics and population, the returns available to Australian sharemarket investors were similar over the two vastly different periods.

Is that what you would have expected? Does that suggest to you we are quite possibly encountering “normal” post market crash returns? I don’t know but I do like being open to many sides of any argument, so feel free to comment or criticise or correct!

Further Reading

- Moneysmart – ASIC’s excellent website for retail investors looking for government guidance on financial basics

- Changes to Australian sharemarket indices – Australian Parliament.

- Sharemarket cycles – Wikipedia (although focused on the USA)

- Sharemarket investment clock – ASX