Risk and Return are two aspects of investment that are most often discussed separately, as if it were possible to have one without the other. This is especially true in the post-Global Financial Crisis (“GFC”) world, where the range of potential outcomes can be quite large. The GFC and its aftermath have created big huge imbalances in the global money system, and this results in a distortion of the risk and return outcomes, as well as a lot of uncertainty for investors as they try to come to grips with unusual circumstances.

Unusual circumstances allow a lot of strange theories to emerge, and make it easy to get confused by the “noise” of day-to-day movements and broader cyclical movements that are just part and parcel of a normally operating market. Given the room for misunderstanding, it’s worthwhile taking a moment to pause and consider some of these issues from a broader perspective. Here are some thoughts on risk and return from my financial planner point of view.

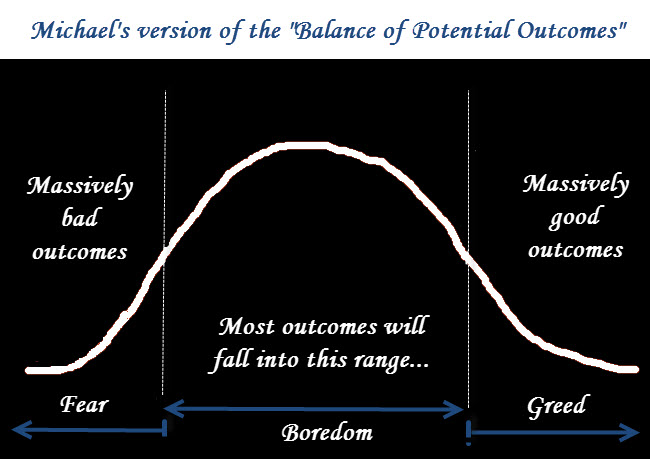

Risk and Return potential outcomes

Here’s the crux of risk and return outcomes, as they are treated by the majority of commentators, news organisations, marketing plans and sales programs. It’s a Michael-version graph of the range of potential outcomes for any given investment or process.

Have a close listen the next time you tune in to a financial update. My guess is that you will find the bulk of discussion and commentary based on the two extreme ends of the range of possible outcomes. That is where the news is and where the most interest is, as it involves our fundamental emotions – fear and greed. Yet the most likely outcomes are going to be in the “middle” range of possibilities. In other words, better than our worst fears but not as good as our most optimistic hopes.

And let’s admit it – that is boring. Most of us don’t really want to know anything about ‘average’ or ‘usual’ or ‘expected’. What stirs our blood is the possibility of doing better, gaining more or being better than average.

Yet anecdotally, we know that such outcomes are less likely to happen. Open any investment magazine or newspaper or website, and you are likely to be confronted by articles and advertisements giving you the insight on how to beat the average. It’s counter-intuitive really, isn’t it? It’s a bit like the studies that show that the average person believes their driving skills are better than average…

“Tail” risk and return

Regular readers will be aware of my affection for the book “Black Swan” by Nassim Taleb. The book discusses the conundrum whereby extremely unlikely events are likely to happen more frequently than standard mathematical probabilities would have us believe. It’s a fascinating look at the outer-end possibilities, and anyone interested in finance and money would do well to read it.

An initial look would suggest that the ideas underlying the “Black Swan” run counter to my graph above. After all, if those tail risks happen more often than expected, surely they will take up more of the graph? Yet this is not necessarily so. Nassim Taleb shows that most people downplay or even ignore the tail risks, often with catastrophic outcomes. However, that doesn’t stop those risks from being “tail” risks – ie, less likely to happen. When they do occur they may have far more impact than expected but again, that does not mean those more extreme outcomes are more likely to occur than “standard” outcomes.

The Global Financial Crisis of 2007 highlighted the extent to which those “tail risks” can interfere with plans and positions and expectations. The very fabric of our global finances was brought into question during this period, and for a brief while things did look very grim indeed. Yet the average eventually exerted itself. Some assets and investments failed completely, yet the experience of most people was less extreme. Many of the assets that fell most during the GFC also recovered strongly in the period since.

The GFC was a torrid time for all investors. It was also a very challenging period for financial planners. As a profession, we tend to keep a focus on longer term outcomes but many long term assumptions were brought into question after 2007. i am old enough to remember the impact of the 1987 sharemarket crash, and the turmoil that it presented to people at the time.

However, in 1987 the market crashed very quickly and in many ways the potential areas of risk were relatively clear. In the 2007 Global Financial Crisis, the sharemarket took well over a year to grind down to its final low point. By that time, fear had become entrenched, and many people were certain that ALL of the old certainties were now failed ideas.

The GFC was really a global banking crisis, which meant the pressures and stresses did not necessarily come from the most obvious places. In other words, the “tail end” risks were elevated and it was particularly difficult to know where problems could emerge. That was borne out when the Euro crisis hit, just as the investment markets were beginning to recover.

Remember when everyone was worried that Greece would go broke? Or that Ireland would follow. Or Portugal, Spain and Italy? Big things did indeed happen – but the actual outcomes were back in the ‘average’. Remember when the United States legislators couldn’t agree on whether or not they would pay the nation’s bills? The possibilities were awful – but the outcome was fairly standard. All sorts of people have predicted dire outcomes from a “hard landing” in China. That may still eventuate but right now the outcomes are looking rather “standard”.

“Tail Risks” today

When reading my note, please remember that there is ALWAYS a large risk of something bad happening, and you only have to look at the newspaper headlines on any given day to see what that may be. Yet todays news often becomes tomorrow’s forgotten story, so any discussion on extreme outcomes or “tail risks” should be considered in this light.

What are today’s “tail risks”. There are always the “left of field” events that nobody saw in advance (although there are always ‘experts’ who come out after to say that they predicted the outcome…) but we can at least list the more obvious possibilities:

- Armed conflict – whether the Middle East, Asia, South America, international or civil revolution.

- 9/11 level terrorist events.

- “Bubbles” bursting – currently the USA long term bond yields are rising in a dramatic fashion, regardless of Reserve Bank money printing to force the opposite outcome. There have been 12 “cases where Baa bond rates went up by 18% or more over 200 days. These periods coincide with events which our collective memory associates with crises. The twelfth incidence of 18% yield moves is occurring now…” (“Of dynamite fishing and whales”, Charles Gave of GaveKal addressing the 2013 Portfolio Construction Forum).

- Protectionism in a major trading nation sparking similar moves globally

- A large currency change in, for example, the US dollar.

- The failure of a large bank that was previously thought to be secure.

- Failure of Greece or a Euro state, leading to Euro instability.

The extreme risks are always a possibility – but care should be taken when assuming that they are always going to happen. For an academic statement of this position, please refer to the Michael bell-curve chart above…

Risk and return – is the GFC finished?

It may seem like a silly question. The Global Financial Crisis started back in 2007 and here we are 6 years later, wondering whether the crisis is finally over?

There are a lot of people who believe that it is – that the GFC is history and we are now in a world that is gradually recovering and returning to ‘normal’. However, there are some who continue to put emphasis on the more extreme potential future outcomes. Here’s one example, a link to a site whereby a commentator lists “13 Reasons Why Gold Will Hit $5000/oz“.

Personally, i don’t think the GFC will be over until the wave of money printed these last few years is absorbed back safely into the system – but that does not mean that i expect the more extreme outcomes to play out. They remain possibilities but are less likely than standard, boring outcomes.

Risk and Return – Global printing of money

Every now and then i come across particularly clear and straight-forward explanations for what would otherwise be quite complex issues. I’ve found one that covers money printing. The central banks of the USA, UK, Europe and Japan have all printed unprecedented amounts of money in an effort to stimulate their economies and stave off or get out of, recession. These are strange times indeed – but there is the possibility that these economies are gradually emerging from the depths of recession and back to a pathway of economic growth. As a result, the money printing will have to be reversed in one way or another. Nobody really knows how that will play out – and therefore we are back to that fear/ boredom/ greed matrix.

It’s not unrealistic to say that all assets across the financial globe are priced from the United States central bank rate. We know that the rate is artificially low – so when it lifts back to “normal” it will have an unknown and most likely, uneven, impact on different areas of the economy. How do we put this range of outcomes into context?

Hamish Douglass is the Chief Executive Officer & Portfolio Manager, Magellan Global Fund. He has recently given a presentation on the post GFC environment, and doesn’t hesitate to look at the potential for bad outcomes. However, he also puts that into context by suggesting that the more likely outcome is an extended and boring return to “normal”. You can see the full presentation material at this link here.

In page 10 of the presentation, Hamish outlines the impact on 10 Year Treasury Bonds if the “tapering” of money printing goes wrong. The example shows that a move upwards to 10% yield (which would be a huge movement) would result in a 47% drop in the value of those bonds. Given that bonds are traditionally held in more conservative portfolios, there is clearly the potential for a big disruption to personal plans and to global economies. As an aged financial planner, i also have vivid memories of the 1994 turmoil in bond markets caused by large increases in official interest rates.

However, there are a lot of people trying very hard to make sure that such things do not happen. Central bankers are not fools – they are vividly aware of the impact of their policies and will do “whatever it takes” to try to bring stability to financial markets. This makes the extreme outcomes even less likely – still possible… just less likely.

So much for the “tail risks”.

Risk and Return – where does “return” come from?

We’ve dwelt on risk quite a bit so far. How about return?

This is where it gets interesting. At least, interesting from a financial planner point of view. Over the years, i have watched a lot of people attempt to reach the higher rates of return by trying such things as day-trading in shares, trading options, gearing into houses and a raft of other measures. Sometimes taking on these extra risks pays off, and sometimes it does not. In my experience, most people attempt these things because they see “standard” forms of investment as being ineffective or expensive or biased or a rip-off or some such issue.

Years of experience suggest to me that the real reason so many people avoid “standard” forms of investment is that they are boring – they don’t involve enough activity (or “doing something”) and they assume that there are “experts” doing a job that they really aren’t that good at.

Now i’m not standing here on my blogsite soapbox to expound the virtues of so-called experts. What i am suggesting though, is that in many cases the search for return can become disconnected from an understanding of risk, and the risks necessary to obtain any given return.

Risk and Return – the boring way will probably do just fine

Here’s a question for you… “How much of your investment outcome is determined by the selection of the particular investment you hold or the market timing for buying and selling that investment?“.

The answer? Vanguard (one of the world’s largest fund managers) has conducted a study “of more than 300 fund managers across 20 years.

It found that asset allocation was responsible for 90% of a diversified portfolio’s return patterns over time. This leaves only 10% for factors such as market timing or securities selection.”

Think about that for a moment. The study is suggesting that it doesn’t matter what you buy or even when you buy – the bulk of your return will be determined by the mix of cash, shares, property and other investments that you hold over that period.

Risk and Return – “buy and hold” actually works…?

This makes sense really. If you buy and sell shares or properties then sometimes you will do very well and sometimes you will not do so well. Over the longer term, the rate of return achieved from the area of investment your money is in (known as “asset class” or “allocation”) matter more than your choice of what to buy or when. In other words, whether you bought shares or property or cash or what-have-you is far more important than whether you bought Newcrest or a CBA term deposit or a property in South Perth. The period post-GFC is a very good example of this idea in practice, and to investigate further we’ll look at the sharemarket.

Immediately following the GFC low-point both financial shares and mining shares staged a strong recovery. However, financial shares were hit heavily by the subsequent Euro crisis and the USA debt ceiling crisis. During this period, mining and materials companies were enjoying boom times, with commodity prices lifting and lots of money being directed towards investment in coal, gold, and iron ore. That position has since reversed again.

It is quite possible that some people picked each trend, and bought just the right assets at just the right times. But the reality is that those people would be in the minority. Most people trying their own hand at investment selection lost at one time and won at the other. The end result is most likely relatively similar. As an example of the difficulty of picking outright winners, who do you know that was out there buying international property assets last year?

The average return for Australian shares in the 10 years to 30th June 2013 was 9.2%. Over 20 years it was 9.5% and over 30 years it was 11.6%. That’s assuming you bought and held on to, a very diverse range of shares that mirrored the All Ordinaries Accumulation Index (assuming you reinvested dividends).

That’s quite a good return. It’s not that much different from the returns achieved from Perth residential property. Remember that return was available from simply buying a big chunk of the market and holding on to it (well, so long as you followed an “index” based strategy but that’s a discussion for another day). What it means is that quite good returns can be achieved by just making the “average” return.

It’s probably not what most people expect. It’s certainly not what most people actually receive – as the bulk of people who buy shares do so on a whim or a fancy or on the recommendation of a friend or a relative or someone “who really knows their stuff”. Long term investing in shares is not something that most people do. It’s also not what a basis for most commentary on shares – which is usually based on the idea of buying at the perfect low point and selling at the perfect high point.

The end result of all this..? Highly active trading may provide a feeling of “doing something” but over multiple business cycles, such trading will have difficulty keeping up with a buy-and-hold strategy, never mind beating it.

Financial Planning “buy and hold” is anything but passive…

Here’s a hugely popular myth that does the rounds of financial commentary on a regular basis – that “buy and hold” is a passive strategy that will see you lose money. There are lots of examples that can be used to show that “buy and hold” will not work but the bulk of those examples involve a selection of individual shares or sectors or whatever. These examples are then used to show you some apparent dangers of ‘doing nothing’. However, most financial planners “like” managed funds and promote the use of managed funds because there is a extremely active management process underlying them. Financial planners look through the managed funds and see the active processes taking place within.

From time to time, an extremely active, professional management process will result in outcomes that are not good at all.

The catch-cry of do-it-yourself commentators in the last few years has been “why give my money to so-called ‘professional managers’ when they just lose you money? You can do that yourself!”. Taking control of your own money in such circumstances sounds like a great idea, and for some people it probably will be.

Most people however, just don’t have the time or don’t want to allocate the time required to continuously watch and alter their investments. My experience over the years is that people who do take control of their finances during times of market stresses or negative returns have trouble keeping interested and active over the longer term. Professional managers however, get up on a Monday morning and go to work to do what they did the week before and what they will do the week after, and that is to use their best knowledge, experience and training in an attempt to generate good outcomes for people, so that their investment expertise gets a better recognition and they have a chance of making more money for themselves.

Professional managers cannot afford the luxury of stopping still or of “doing nothing”. They would eventually lose their job, their income and their reputation.

Even “passive” managers are very active

Back to the passive/active business. If you buy the standard “managed fund” and hold it for a while – you are undertaking a very “passive” strategy – but only from your personal point of view. You receive annual or quarterly updates, and maybe you log-in to check balances from time to time. Your role is mainly to hand over some cash and to watch and wait to see what happens to it. That can leave you feeling detached or un-involved with what is going on with your hard earned dollars BUT that does not mean your money or the people managing it are doing nothing. Quite the contrary. Here’s what is going on under the skin of that professionally managed fund – and i’m going to be very brief, so take it that there is an awful lot else going on as well:

- Strategy – there will be a highly specific “terms of reference” under which that fund operates. Sometimes called an “investment mandate”, this document will have been exhaustively researched and regularly updated to ensure the fund remains competitive in a changing investment environment.

- Monitoring – The strategy will generally define under what conditions assets are bought, held or sold. This requires continuous monitoring of the portfolio against these guidelines.

- Buying/selling – The average managed fund in shares will “turn over” their total value every year or so. It is only a few “high value” fund managers who have low turnover (buying and selling) in a managed share fund. This does not mean wholesale buying and selling of entire holdings. Rather, the manager will tend to increase or decrease their exposure based on performance and outcomes measured against the overall investment mandate or strategy.

- Tax management – Some funds are better than others at this. Working out when to take a loss or profit and the impact of tax is a big effort.

- Cost management. Fund managers will find every little cost saving they can in an effort to ensure that the continuous turnover does not result in an increase in overall costs to investors – it is NOT a common thing for fund managers to lift their fees… Australia’s money management industry is too competitive to forgive very much of that activity!

- Research, research and more research – In a competitive world, every little bit of information or knowledge can have an impact. A lot of fund managers spend a lot of time and money visiting the companies they invest in, as well as keeping up to date with the latest investment research.

.This is not to say that a professional fund manager will be able to do all this and result in a better outcome than an individual undertaking their own research and trading activity. All i am saying is that the “buy-and-hold” strategy put forward by many financial advisers involves a lot of activity that is simply not visible to the investor. In effect, extremely fluid and dynamically active strategies will come across as boring and staid and not worth the money they cost – but it ain’t necessarily so…

Musing on risks and returns

The financial planner story is predominantly a boring one. It involves spreading your money around and trying not to pick individual winners if you can help it. It also involves taking a longer term view, and trying to ignore the “noise” of day or the week or the month. For financial planners, the real issues are broader. Should you be investing at all? What are your expectations, and how do they stack up against possibilities?

This is not to say that financial planners always get things right – quite simply, they do not. It would be a long bow to draw indeed, if you were to suggest any such outcome. Extreme events can happen, and when they do it is usually not obvious beforehand just where these events will appear. For all their knowledge, experience and training, financial planners are still prone to extreme event outcomes. If you want proof of this just consider the Long Term Capital Management experience, in which incredibly knowledgeable and experienced professional managers, recognised at a global level, made mistakes large enough to tilt global finances near the abyss. Or the many professional investment managers who failed to input into their models the possible scope of changes that occurred in the GFC.

Extreme outcomes are always a possibility. However, care should be taken that you do not begin to believe that only extreme outcomes will happen. In difficult or strange times many people will try to convince you that extreme outcomes are just around the corner. They may be right but in most cases, the world of money reverts to its long term averages. The key is to try to make sure that you can stay your course long enough to benefit from that.

Michael’s basics of risk and return

In any look at risk and return, it is worthwhile going back to the most basic of basics:

- Cash is the only secure investment but it does not mean that it is free of risk.

- Even cash can be insecure, if large institutions fail through risky ventures, fraud, negligence or extreme market events. Remember, cash in the bank is really an investment into the investments, loans and assets of the bank and the hoped-for promise of government support if all else fails.

- Lack of access (liquidity) equals increased risk. It doesn’t matter whether you are talking about term deposits, venture capital investment pools or securitised property. If your money is not available for a longer period of time then there is a risk involved. Usually this risk is compensated for by a higher ongoing yield – but not always.

- Aiming for anything above a “market rate of return” after fees is going to result in an increased risk of ending up with a lower than average market rate of return.

- Once you leave the security of short term cash, you lose control of the value of your capital. Any guarantee or protection that suggests otherwise is really just a shift in that risk.

- “Averages” can be anything but average.

- Today’s “rule” can often become tomorrow’s “error”. Just look at the discussion and analysis of listed versus unlisted property trusts pre/during/post the global financial crisis.

- There is absolutely, categorically NO WAY OF PREDICTING THE FUTURE.

- Boring is often a pretty good pathway, even if wildly uninteresting.

Disclaimer : Remember that nothing in this site is to be taken as personal advice. It is general musings only, and doesn’t really even qualify as general advice. You must not take any part of this website content as a direction to buy or hold or sell anything. That would be personal advice, and i simply do not provide that through this site.

Disclaimer #2 : When i use the term “financial planner” please remember that i am being very generic. i have covered in earlier posts just how diverse are the areas of expertise and knowledge and activity that financial planners in Australia operate in. Some planners never use managed funds, and others don’t even want to invest your money. These are just musings of my thoughts of risk and return as it applies in the “standard” world of financial planning.