The Reserve Bank of Australia today announced that it has dropped interest rates yet again. Borrowers on variable rates linked to the RBA cash rate will rejoice when their particular financial institution eventually agrees to pass on the interest rate cut. Pensioners and people living off interest income will find their next interest payment is even lower, causing many to wonder what they can do in the face of such low interest rates.

RBA drops interest rates – why?

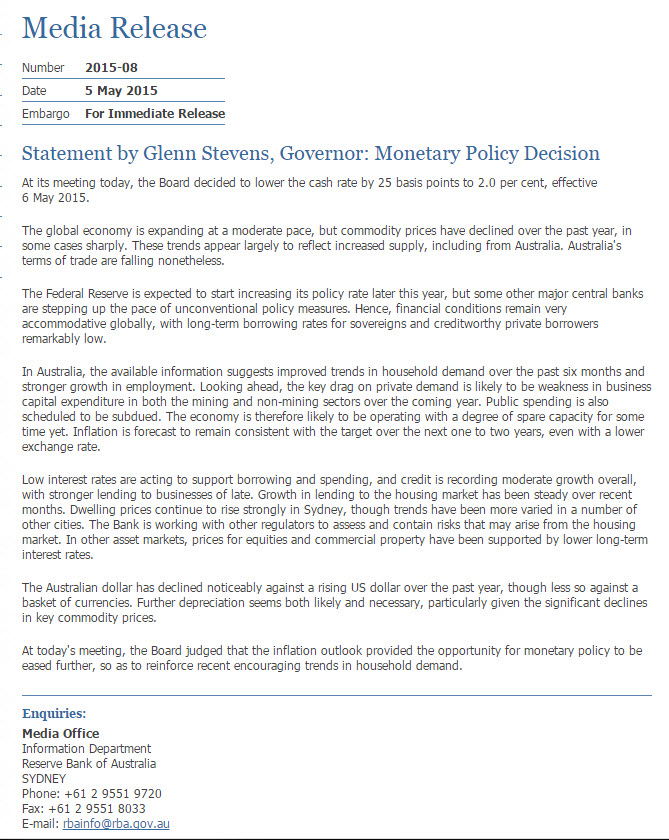

The “why?” is easily answered at the superficial level. You only have to read the RBA’s minutes that are released with the interest rate announcement. You can find it on the RBA website media statement on RBA interest rate decision.

RBA drops interest rates – while they are rising?

Wait a minute Michael – the media announcement tells us that “In other asset markets, prices for equities and commercial property have been supported by lower long-term interest rates” – so how can you say that they are rising?

Well… i can say that because that is what they are doing. At any given time there is usually a range of interest rates out there – ranging from the short term rates set off the RBA cash rate through to longer term rates for government or institutional debt securities. Long term debt is priced in those long term pools. The government may raise money from a debt security but it will quickly be repriced by the market, so governments have far less power over the longer term rates. If you buy my proposition that the world benchmark’s its interest rates from the multi-trillion dollar pool of US debt securities then here is what has been happening to longer term rates in the United States of late..

In this case, i’ve charted the yield for US securities 10 year bonds.While the yield has jumped around quite a bit, you wouldn’t exactly look at this chart and say that long term rates are falling. While Australian longer term government securities remain at elevated levels, and therefore are showing very low interest yields, the very recent prices for longer dates securities has fallen a little from recent highs. An example would be to look at the ASX listed security GSIQ30 – which is a listing of the Australian government indexed debt security maturing 20 September 2030. The security does not trade every day but pricing at the moment is about 5% below its recent highs, which indicates the effective interest rate from those securities for recent purchasers has been lifting.

The RBA knows that interest rates are expected to rise in the USA later in the year, and that will have some impact on Australia’s interest rates as well. Rate rises in the USA are of particular interest for Australian rates right now, as the “premium” of our rates over theirs has recently shrunk to its lowest level in a long time – and that leaves Australia exposed to a “double-whammy” effect if the marketplace takes that premium back to its historical average at the same time that the US raises their rates.

None of this would stop a current interest rate, as the RBA could just as easily lift rates again in a few short months – but you would have to ask why interest rates are being dropped to historically low levels right now?

RBA drops interest rates – but should it?

Here’s my angst at watching these interest rate movements. It’s not the RBA or even the central bankers around the world who have resorted to experimental monetary policy such as “Quantitative Easing” and other forms of money printing, who make this financial planner wince. It’s the likelihood that central bankers are having to resort to extreme money policies in an effort to keep economies stable – mainly because governments are failing to put in place policies that stimulate long term growth or allocate resources efficiently. Here’s an example of this in action. We’ll refer to comments from AMP Capital’s chief economist Shane Oliver, as reported in the news.com.au article “RBA cuts interest rate to historic low” here.

AMP Capital chief economist Dr Shane Oliver said the RBA’s case for a cut was strong given weak business investment outlook, falling commodity prices and a still too-high Australian dollar.

“While there was some speculation the RBA would keep rates on hold due to fears of fuelling bubble-like conditions in the Sydney housing market, Dr Oliver said the central bank had largely passed on the baton of slowing property investment to the Australian Prudential Regulation Authority.

“The Reserve Bank was worried that bubble-like conditions could inflate further and that could result in financial instability down the track,” he said. “But it’s dangerous to set monetary policy based on one city.”

The cut will be welcomed by Australians with home loans, personal loans and credit card debt, but self-funded retirees relying on interest from bank deposits may feel the pinch. “Australians owe the banks about $2 trillion in loans, while there are about $800 billion worth of bank deposits,” Dr Oliver said. “Obviously one swamps the other.”

The record-low cash rate was a sign that the economy was still in trouble, Dr Oliver said. “The clear message is the economy is still not performing as well as it should and needs a bit of help in the rebalancing process. Growth is still running below trend, and the period for below-trend growth keeps getting pushed out.”

Lower interest rates should help drive down the value of the dollar, giving a much-needed boost to industries like tourism, manufacturing, agriculture and higher education.”

Australia’s governments have failed to implement effective nation-building infrastructure projects, which could have helped to moderate the falls in mining and associated industry investment. Not replaced mind you but a simple moderation effect. And that would help cushion workers and industry from the impact of large falls in commodity prices and the ensuing cancellation or deferral of projects. Infrastructure also benefits from needing the same style of construction, design and work skills as many large mining projects. But instead, Australia’s government embarks on an austerity program in an effort to reign in debt levels.

The May 2015 Federal Budget is expected to set out details of Australia’s return to a surplus. National debate on government finances appears to have been hijacked by those who believe our debt is “out of control” and that the country needs to “return” to a surplus. Frankly, i find that silly. Australia has a growing population, and a need to put in place the infrastructure to support that growing population. There is nothing wrong with moving into deficit if the purpose is to improve productivity or increase the nation’s capacity for productivity or output into the future. That’s a simple invest for growth story.

Low interest rates aren’t going to make their way into investment if businesses and workers don’t feel secure about their futures. It really is as simple as that. Build a more secure vision of the future, and clarify the pathway to getting there, and people will spend and invest and work harder to make sure they enjoy their share of that future. But that is not spirit of the time – “zeitgeist” – that exists in media and social commentary at the moment. Instead it’s all about fear and worry about all manner of things.

RBA drops interest rates – a currency war?

It is always possible to argue that changes in currencies are simple reactions to standard environmental factors. On that basis, there never will be a “currency war” as each nation simply adjusts its interest rates and currency intervention in order to meet benchmarks of one kind or another. Yet traditional economics tells us that there are such things as currency wars, and that they do count for a great deal as a currency war could end in a trade war which could restrict trade and the free movement of goods and capital, resulting in inefficiencies and higher costs. So we should ask ourselves whether Australia has entered some form of currency war in an effort to impact on the relative value of our dollar?

Alan Kohler certainly thinks so. Here’s his article “The RBA races into the currency war” on ABC’s “The Drum”. And world recognised economist Nouriel Roubini is very vocal on the negative impacts of currency wars, and you can read his relatively short but excellent article “The dollar joins the currency wars” here.

Another global financial heavy-weight with an opinion is El-Erian, Chief Economic Adviser at Allianz and a member of its International Executive Committee. He is Chairman of President Barack Obama’s Global Development Council, and he previously served as CEO and co-Chief Investment Officer of PIMCO. In an article on the project-syndicate.org website, El-Erian is keen to point out the difficulties of central bankers attempting to impact currency, and take on part of the job that should be handled by proficient governments.

For starters, central banks cannot deliver the structural components – for example, infrastructure investments, better-functioning labor markets, and pro-growth budget reforms – needed to drive robust and sustained recovery. Nor can they resolve the aggregate-demand imbalance – that is, the disparity between the ability and the willingness of households, companies, and governments to spend. And they cannot eliminate pockets of excessive indebtedness that inhibit new investment and growth.

It is little wonder, then, that monetary-policy instruments have become increasingly unreliable in generating economic growth, steady inflation, and financial stability. Central banks have been forced onto a policy path that is far from ideal – not least because they increasingly risk inciting some of the zero-sum elements of an undeclared currency war. With the notable exception of the Fed, central banks fear the impact of an appreciating currency on domestic companies’ competitiveness too much not to intervene; indeed, an increasing number of them are working actively to weaken their currencies.

The “divergence” of economic performance and monetary policy among three of the world’s most systemically important economies – the eurozone, Japan, and the United States – has added another layer of confusion for the rest of the world, with particularly significant implications for small, open economies. Indeed, the surprising actions taken by Singapore and Switzerland were a direct response to this divergence, as was Denmark’s decision to halt all sales of government securities, in order to push interest rates lower and counter upward pressure on the krone.

Read more at http://www.project-syndicate.org/commentary/monetary-policy-central-bank-activism-by-mohamed-a–el-erian-2015-02

Some commentators would like to see the RBA hold off on interest rate cuts (“RBA should resist pressure to cut interest rates” The Australian) but in the end, the RBA has to do what it thinks best or most likely to achieve its mandates for stability, the currency and employment, among other things. For those interested in such things, here is the RBA purpose statement from its website..

The Reserve Bank of Australia (RBA) is Australia’s central bank and derives its functions and powers from the Reserve Bank Act 1959. Its duty is to contribute to the stability of the currency, full employment, and the economic prosperity and welfare of the Australian people. It does this by setting the cash rate to meet an agreed medium-term inflation target, working to maintain a strong financial system and efficient payments system, and issuing the nation’s banknotes. The RBA provides certain banking services as required to the Australian Government and its agencies, and to a number of overseas central banks and official institutions. Additionally, it manages Australia’s gold and foreign exchange reserves.

So what’s your problem, Michael?

Tokenism is my problem.

It appears to me that governments and policymakers have a fairly good idea of what is required to boost employment, foster growth and provide the kinds of services likely to be required by a growing population. It’s just that they can’t seem to set policy or make decisions in ways strong enough to meet those targets. Instead, the large changes required to keep Australia competitive and thriving seem to be put aside in favour of small, more acceptable “token” gestures that avoid tackling the real issues.

Central bankers have their hands tied, as they are not allowed to be political and commenting on government policy would be seen as political. Pity. But it doesn’t stop them from making a few side comments of dropping a few hints that interest rates aren’t all that effective in dealing with the post Global Financial Crisis world.

Here’s an excerpt from an article from last year “Stimulating Australia – why lower interest rates may not be the answer” on the Australian website of the Guardian.

Perhaps we are asking too much of monetary policy.

The deputy governor, Dr Philip Lowe, noted that “at the end of the day, monetary policy cannot be the engine of growth in the economy. We can help smooth out the fluctuations, but we cannot in the end drive the overall growth in the economy”. Instead he suggests “we need to invest more, and more effectively, in education, in human capital accumulation and in infrastructure. Risk taking, education and infrastructure are the things that are going to help us be a high-wage, high-productivity, high value-added economy.”

My other problem is that using interest rates to foster investment and growth pays scant attention to the fickle nature of interest rate levels. In other words, excessively low rates may encourage or even force some people to borrow more than they reasonably should or to spend more or make assumptions that have a very good chance of being very wrong. RBA Governor Glenn Stevens recently highlighted that interest rates were the “lowest in human history” and went on to suggest that low rates will be here for some time and that investors will need to take account of this (my interpretation – another Guardian article covers the comments here). But what if they are not? What if rates start to increase, and increase rapidly? It’s a scenario not being put forward by a lot of people right now but then a lot of people believed that home lending in the USA in 2007 was on very good footing, and we all know how wrong that turned out to be. The post-GFC world in my opinion is excessively risk-averse, with the result that future timelines are shortened, and longer term outcomes are seen only in the light of current trends. But that is another issue for another post on another day…

So the RBA drops interest rates in the hope of stimulating business to borrow to invest or for people to borrow to buy stuff or for investors to borrow to buy houses (although they don’t really want people in Sydney or Melbourne to buy more houses).

What do you think?

Is that really likely to happen?

Are you going to spend more money or borrow more money because the interest rates have temporarily moved by 0.25%?

Notes and further reading